ARIMA Modeling

AutoRegressive Integrated Moving Average

Install Packages

library(readxl)

library(lmtest)

library(forecast)

library(FitAR)

library(fUnitRoots)

Import Data Set

table2 <- read_excel("Datum/1 SCOPUS/2022/Feb-01/Data/table2.xlsx",sheet = "Sheet2")

View(table2)

summary(table2)

avg_jual avg_beli

Min. : 8808 Min. : 8766

1st Qu.:13498 1st Qu.:13480

Median :14190 Median :14078

Mean :13979 Mean :13800

3rd Qu.:14705 3rd Qu.:14257

Max. :15753 Max. :15020

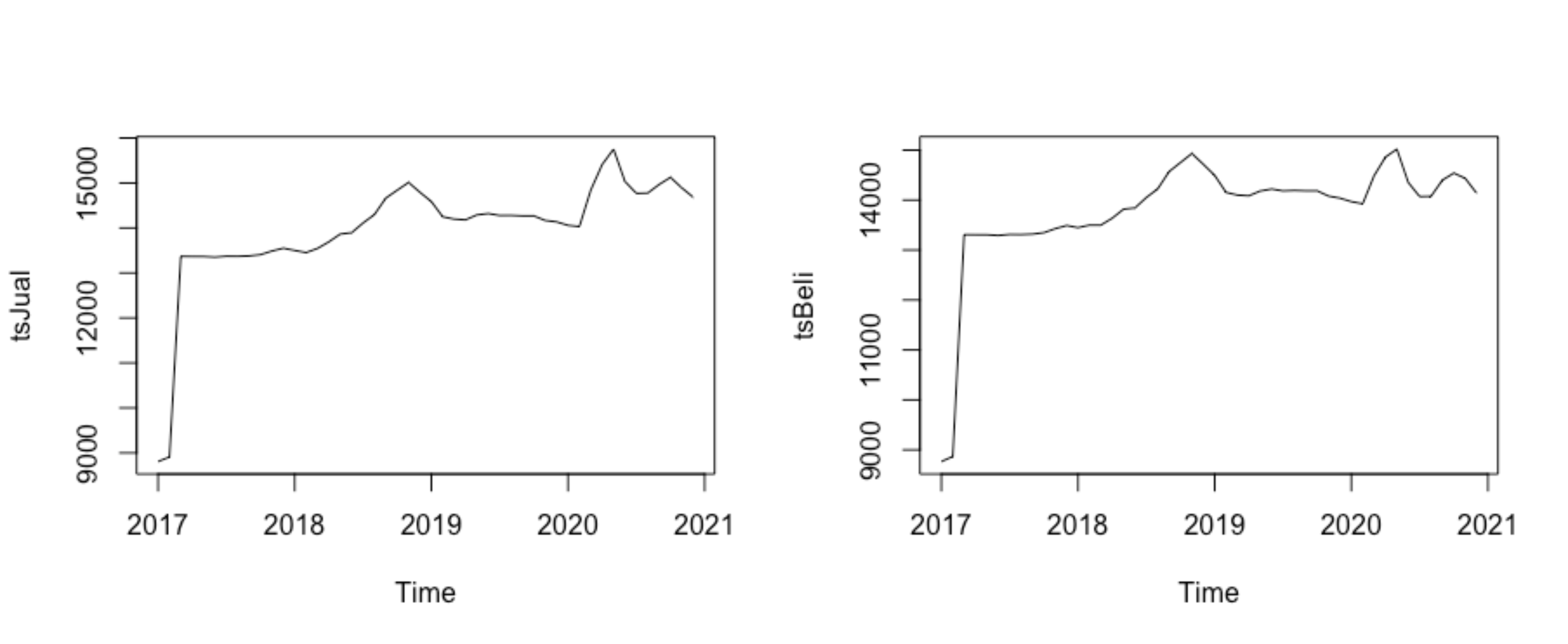

tsJual = ts(table2$avg_jual, start = c(2017,1), frequency = 12)

plot(tsJual)

tsBeli = ts(table2$avg_beli, start = c(2017,1), frequency = 12)

plot(tsBeli)

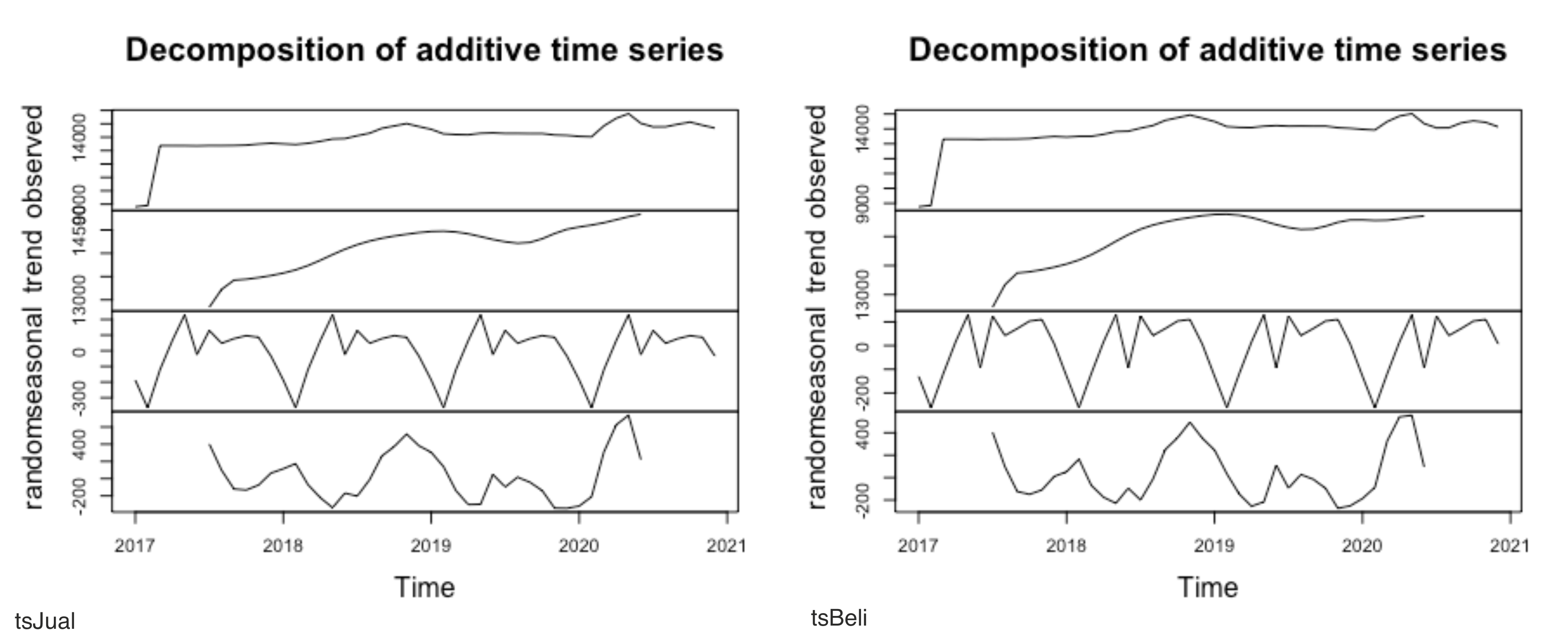

components.tsJual = decompose(tsJual)

plot(components.tsJual)

components.tsBeli = decompose(tsBeli)

plot(components.tsBeli)

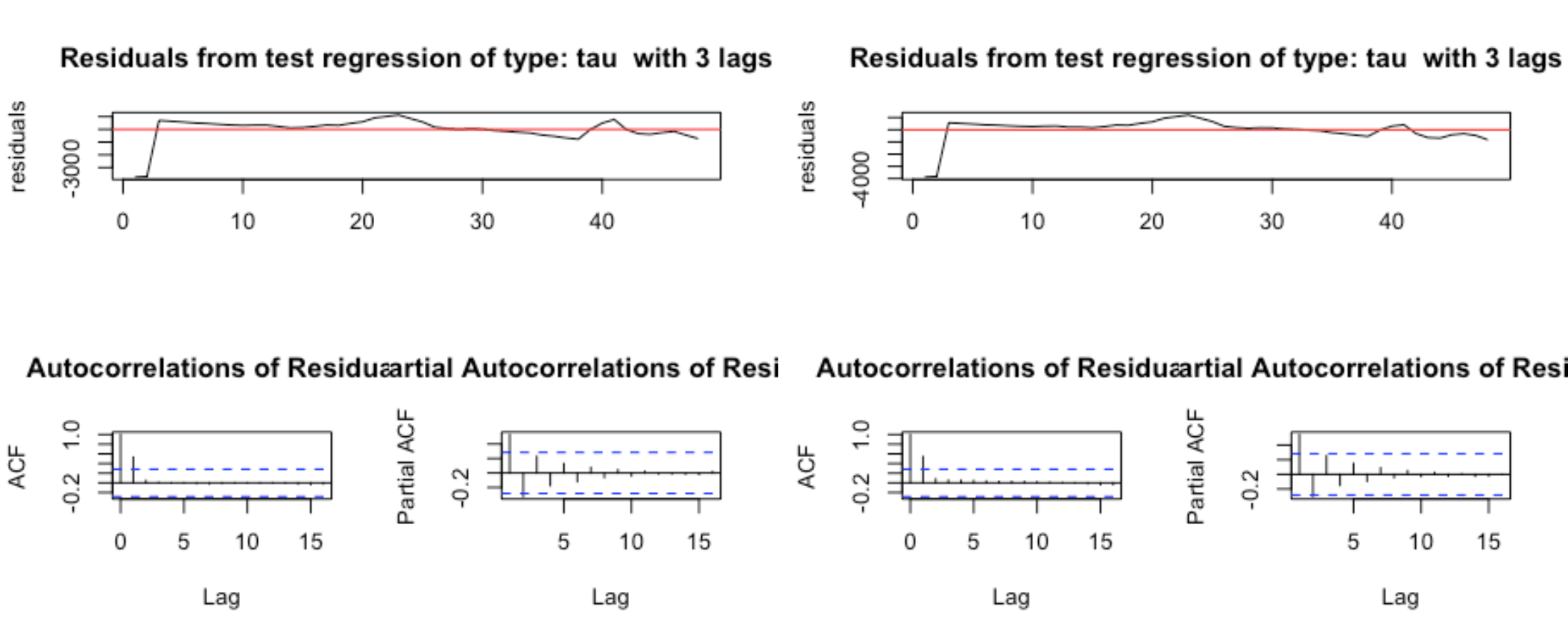

urkpssTest(tsJual, type = c("tau"), lags = c("short"),use.lag = NULL, doplot = TRUE)

urkpssTest(tsBeli, type = c("tau"), lags = c("short"),use.lag = NULL, doplot = TRUE)

sstationary_Jual = diff(tsJual, differences=1)

plot(tsstationary_Jual)

tsstationary_Beli = diff(tsBeli, differences=1)

plot(tsstationary_Beli)

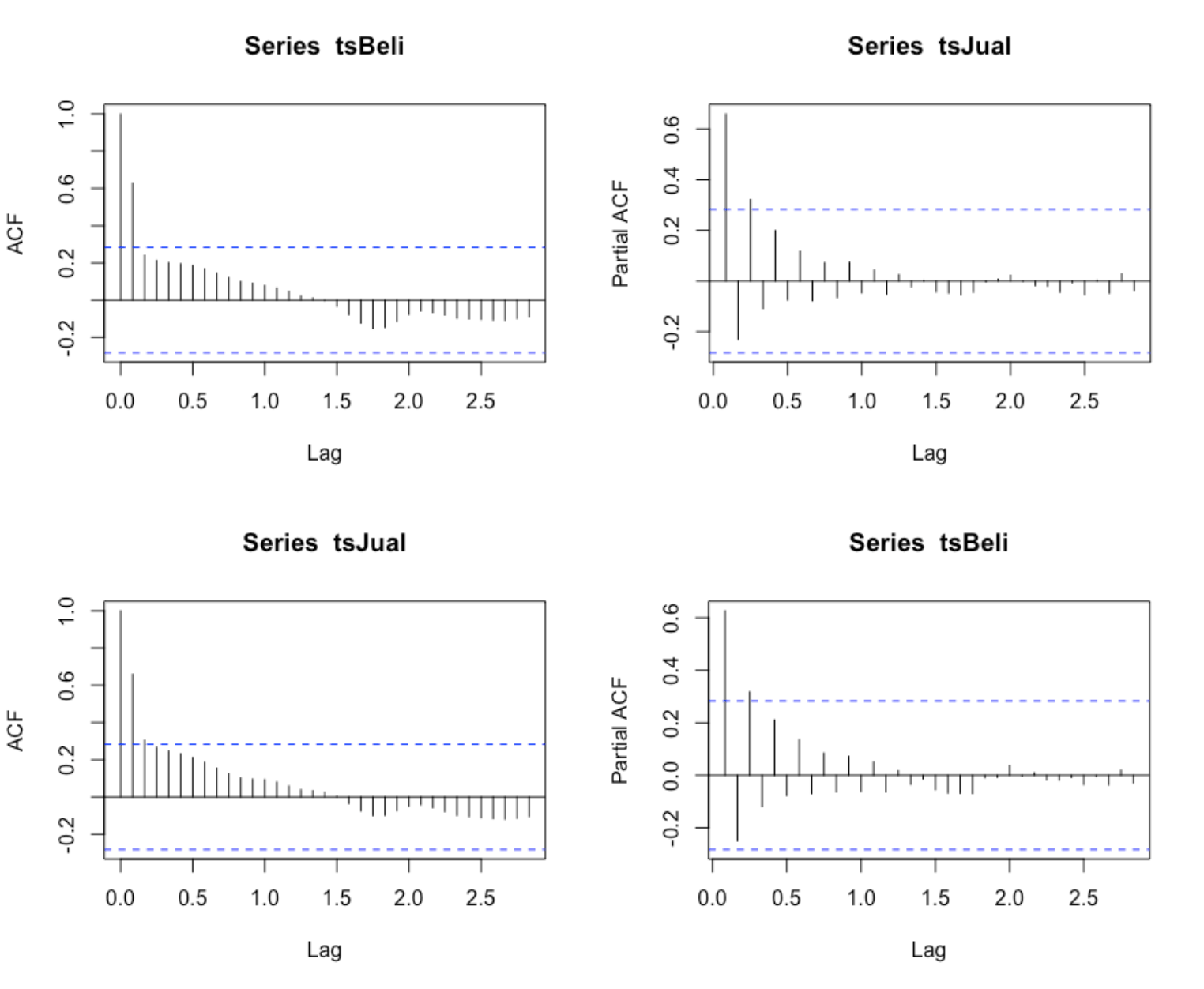

acf(tsJual,lag.max=34)

acf(tsBeli,lag.max=34)

Pacf(tsJual,lag.max=34)

Pacf(tsBeli,lag.max=34)

timeseriesseasonallyadjusted_Jual <- tsJual- components.tsJual$seasonal

tsstationary_Jual <- diff(timeseriesseasonallyadjusted_Jual, differences=1)

timeseriesseasonallyadjusted_Beli <- tsJual- components.tsBeli$seasonal

tsstationary_Beli <- diff(timeseriesseasonallyadjusted_Beli, differences=1)

plot(timeseriesseasonallyadjusted_Beli)

plot(timeseriesseasonallyadjusted_Jual)

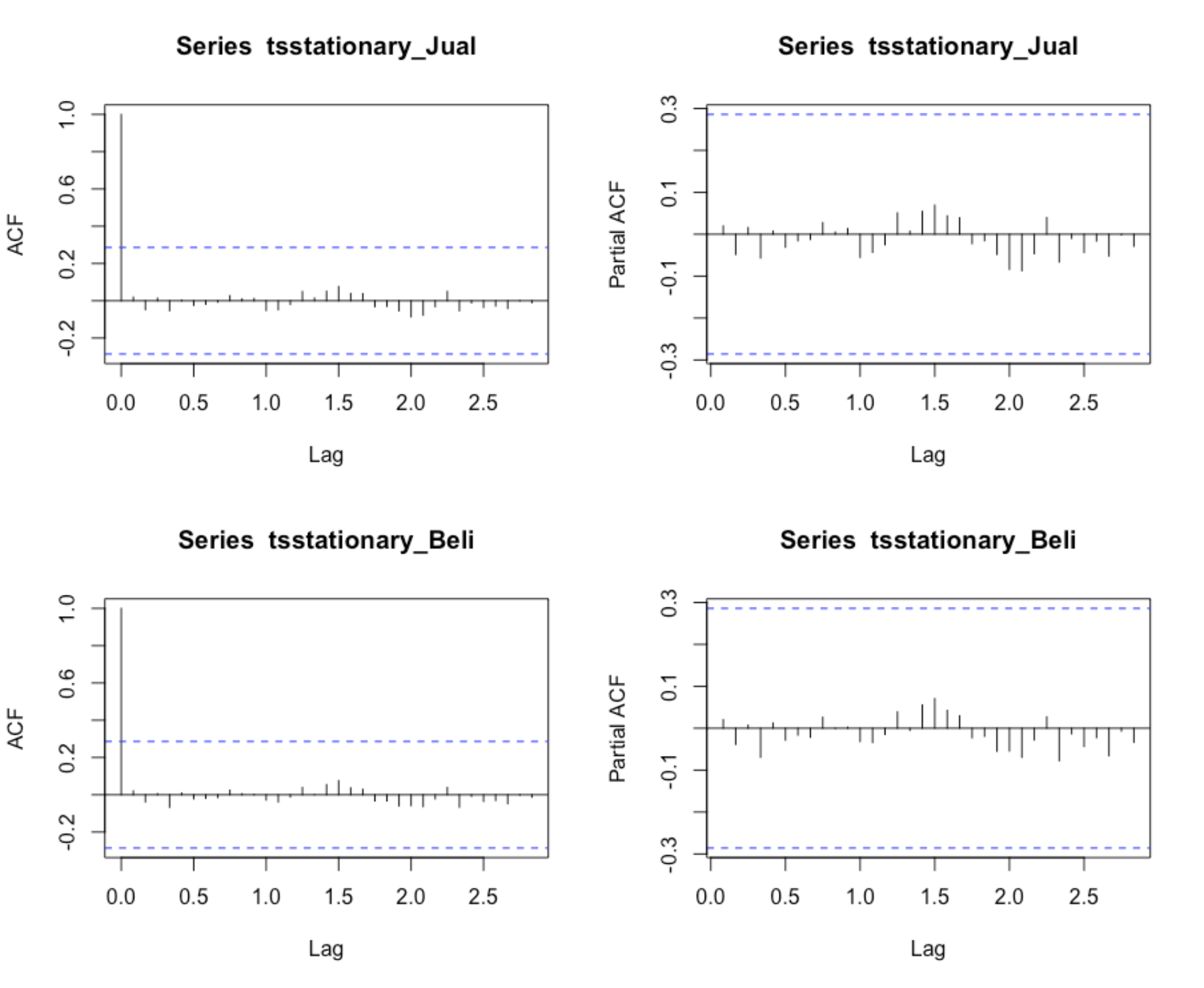

acf(tsstationary_Jual, lag.max=34)

pacf(tsstationary_Jual, lag.max=34)

acf(tsstationary_Beli, lag.max=34)

pacf(tsstationary_Beli, lag.max=34)

fitARIMA_Jual <- arima(tsJual, order=c(1,1,1),seasonal = list(order = c(1,0,0), period = 12),method="ML")

fitARIMA_Beli <- arima(tsBeli, order=c(1,1,1),seasonal = list(order = c(1,0,0), period = 12),method="ML")

coeftest(fitARIMA_Jual)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 -0.021344 1.837953 -0.0116 0.9907

ma1 0.083561 1.842706 0.0453 0.9638

sar1 0.072859 0.274394 0.2655 0.7906

coeftest(fitARIMA_Beli)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.0032167 0.6907733 0.0047 0.9963

ma1 0.0509199 0.7058832 0.0721 0.9425

sar1 -0.0026367 0.3522116 -0.0075 0.9940

fitARIMA_Jual

Call:

arima(x = tsJual, order = c(1, 1, 1), seasonal = list(order = c(1, 0, 0), period = 12),

method = "ML")

Coefficients:

ar1 ma1 sar1

-0.0213 0.0836 0.0729

s.e. 1.8380 1.8427 0.2744

sigma^2 estimated as 472215: log likelihood = -373.76, aic = 755.51

fitARIMA_Beli

Call:

arima(x = tsBeli, order = c(1, 1, 1), seasonal = list(order = c(1, 0, 0), period = 12),

method = "ML")

Coefficients:

ar1 ma1 sar1

0.0032 0.0509 -0.0026

s.e. 0.6908 0.7059 0.3522

sigma^2 estimated as 457012: log likelihood = -372.95, aic = 753.91

confint(fitARIMA_Beli)

2.5 % 97.5 %

ar1 -1.3506740 1.3571074

ma1 -1.3325858 1.4344256

sar1 -0.6929589 0.6876854

confint(fitARIMA_Jual)

2.5 % 97.5 %

ar1 -3.6236644 3.5809772

ma1 -3.5280769 3.6951992

sar1 -0.4649435 0.6106622

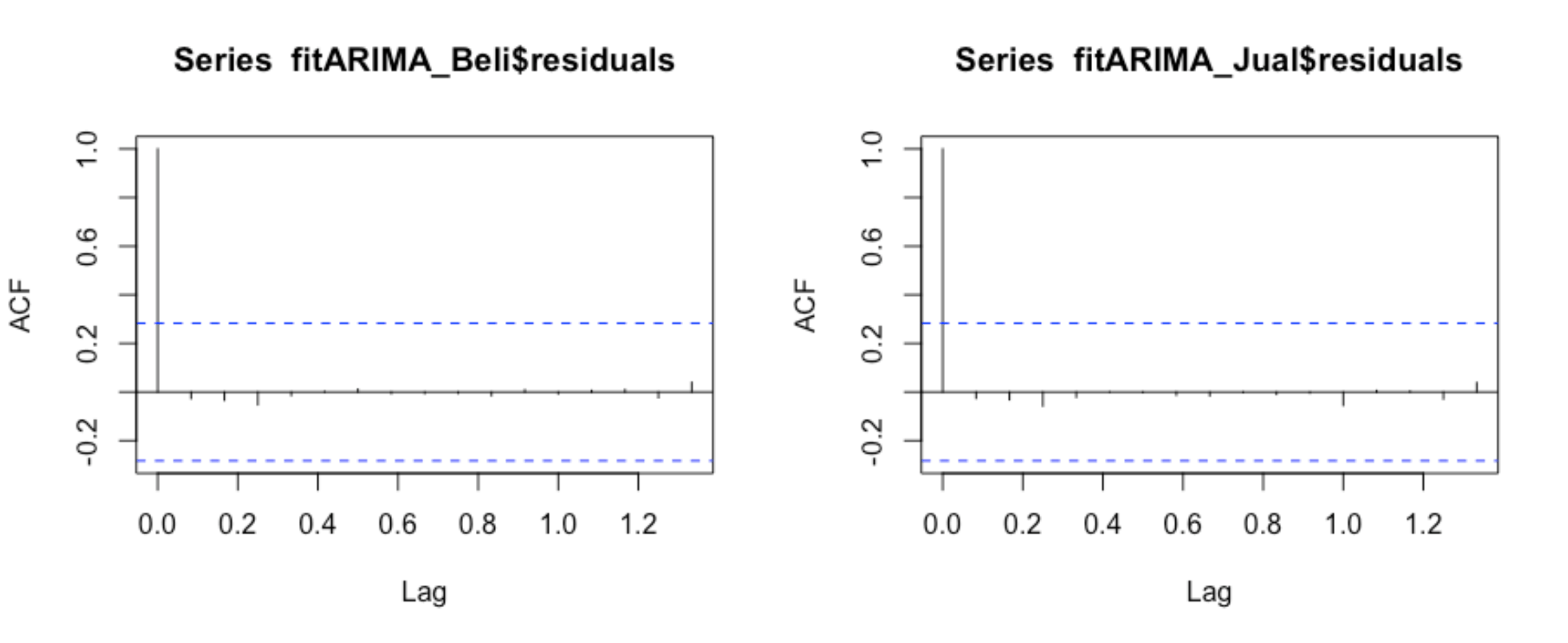

acf(fitARIMA_Beli$residuals)

acf(fitARIMA_Jual$residuals)

boxplot(fitARIMA_Jual$residuals,k=2,StartLag=1)

LjungBoxTest(fitARIMA_Jual$residuals,k=2,StartLag=1)

boxplot(fitARIMA_Beli$residuals,k=2,StartLag=1)

LjungBoxTest(fitARIMA_Beli$residuals,k=2,StartLag=1)

qqnorm(fitARIMA_Jual$residuals)

qqline(fitARIMA_Jual$residuals)

qqnorm(fitARIMA_Beli$residuals)

qqline(fitARIMA_Beli$residuals)

arima(tsJual)

Call:

arima(x = tsJual)

Coefficients:

intercept

13978.5625

s.e. 177.7277

sigma^2 estimated as 1516180: log likelihood = -409.67, aic = 823.34

arima(tsBeli)

Call:

arima(x = tsBeli)

Coefficients:

intercept

13800.3958

s.e. 165.1939

sigma^2 estimated as 1309870: log likelihood = -406.16, aic = 816.32

auto.arima(tsJual, trace=TRUE)

ARIMA(2,1,2)(1,0,1)[12] with drift : Inf

ARIMA(0,1,0) with drift : 750.4713

ARIMA(1,1,0)(1,0,0)[12] with drift : 755.0944

ARIMA(0,1,1)(0,0,1)[12] with drift : 755.0899

ARIMA(0,1,0) : 749.8579

ARIMA(0,1,0)(1,0,0)[12] with drift : 752.7432

ARIMA(0,1,0)(0,0,1)[12] with drift : 752.7402

ARIMA(0,1,0)(1,0,1)[12] with drift : Inf

ARIMA(1,1,0) with drift : 752.7152

ARIMA(0,1,1) with drift : 752.7136

ARIMA(1,1,1) with drift : Inf

Best model: ARIMA(0,1,0)

Series: tsJual

ARIMA(0,1,0)

sigma^2 = 475492: log likelihood = -373.88

AIC=749.77 AICc=749.86 BIC=751.62

auto.arima(tsBeli, trace=TRUE)

ARIMA(2,1,2)(1,0,1)[12] with drift : Inf

ARIMA(0,1,0) with drift : 748.9614

ARIMA(1,1,0)(1,0,0)[12] with drift : 753.5961

ARIMA(0,1,1)(0,0,1)[12] with drift : 753.5933

ARIMA(0,1,0) : 748.1365

ARIMA(0,1,0)(1,0,0)[12] with drift : 751.2314

ARIMA(0,1,0)(0,0,1)[12] with drift : 751.2295

ARIMA(0,1,0)(1,0,1)[12] with drift : 753.6222

ARIMA(1,1,0) with drift : 751.2183

ARIMA(0,1,1) with drift : 751.2173

ARIMA(1,1,1) with drift : Inf

Best model: ARIMA(0,1,0)

Series: tsBeli

ARIMA(0,1,0)

sigma^2 = 458392: log likelihood = -373.02

AIC=748.05 AICc=748.14 BIC=749.9

fitARIMA_Jual

Call:

arima(x = tsJual, order = c(1, 1, 1), seasonal = list(order = c(1, 0, 0), period = 12),

method = "ML")

Coefficients:

ar1 ma1 sar1

-0.0213 0.0836 0.0729

s.e. 1.8380 1.8427 0.2744

sigma^2 estimated as 472215: log likelihood = -373.76, aic = 755.51

fitARIMA_Beli

all:

arima(x = tsBeli, order = c(1, 1, 1), seasonal = list(order = c(1, 0, 0), period = 12),

method = "ML")

Coefficients:

ar1 ma1 sar1

0.0032 0.0509 -0.0026

s.e. 0.6908 0.7059 0.3522

sigma^2 estimated as 457012: log likelihood = -372.95, aic = 753.91

predict(fitARIMA_Jual,n.ahead = 1)

$pred

Jan

2021 14665.9

$se

Jan

2021 687.1792

predict(fitARIMA_Beli,n.ahead = 1)

$pred

Jan

2021 14122.35

$se

Jan

2021 676.0263

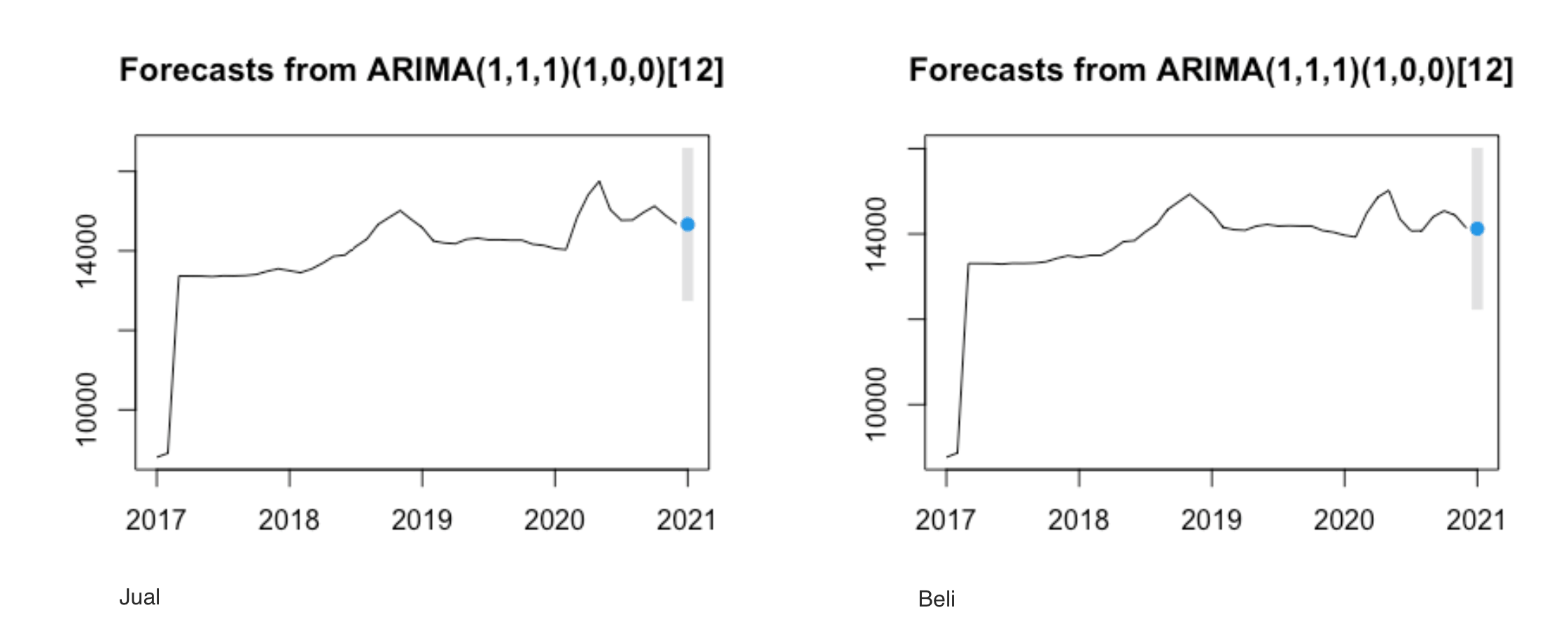

futurVal_Beli <- forecast(fitARIMA_Beli,h=1, level=c(99.5))

futurVal_Jual <- forecast(fitARIMA_Jual,h=1, level=c(99.5))

plot(futurVal_Beli)

plot(futurVal_Jual)

summary(futurVal_Jual)

Forecast method: ARIMA(1,1,1)(1,0,0)[12]

Model Information:

Call:

arima(x = tsJual, order = c(1, 1, 1), seasonal = list(order = c(1, 0, 0), period = 12),

method = "ML")

Coefficients:

ar1 ma1 sar1

-0.0213 0.0836 0.0729

s.e. 1.8380 1.8427 0.2744

sigma^2 estimated as 472215: log likelihood = -373.76, aic = 755.51

Error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 107.4817 679.9846 237.3794 0.794616 1.695755 0.2583878 -0.02594214

Forecasts:

Point Forecast Lo 99.5 Hi 99.5

Jan 2021 14665.9 12736.97 16594.84

summary(futurVal_Beli)

Forecast method: ARIMA(1,1,1)(1,0,0)[12]

Model Information:

Call:

arima(x = tsBeli, order = c(1, 1, 1), seasonal = list(order = c(1, 0, 0), period = 12),

method = "ML")

Coefficients:

ar1 ma1 sar1

0.0032 0.0509 -0.0026

s.e. 0.6908 0.7059 0.3522

sigma^2 estimated as 457012: log likelihood = -372.95, aic = 753.91

Error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 106.293 668.9485 220.1657 0.7954476 1.599417 0.2807839 -0.02688605

Forecasts:

Point Forecast Lo 99.5 Hi 99.5

Jan 2021 14122.35 12224.72 16019.98